In 2025, Europe remained at the forefront of the electric vehicle transition, with EVs accounting for more than a quarter of all new car registrations. In 2026, governments continue to invest heavily in charging networks and zero-emission mandates, but progress is uneven. While Norway and Sweden are close to a full phase-out of petrol cars, electric models still represent less than 10% of new sales in some parts of Southern and Eastern Europe.

The internal combustion engine continues to rule most European countries, even as the EU prepares to end sales of new petrol and diesel cars by 2035. For now, only a few nations, led by the Nordics, are close to fully replacing hydrocarbon-based fuels with greener alternatives. Curious to track the global demand for electric cars, the team at Tradingpedia examined the sales and new registrations figures throughout 2025 from the European Automobile Manufacturers’ Association (ACEA) to reveal which nations lead in EV adoption.

Data shows that across Europe, the growth of battery-electric vehicles (BEVs) has slowed in 2025, due to a range of factors including reduced subsidies and infrastructure challenges. In contrast, plug-in hybrid electric vehicles (PHEVs) are gaining traction, with sales up 33%, while hybrid-electric vehicles (HEVs) continue to grow in popularity. HEVs now hold the largest share of the market at 34.4% of all new car registrations, compared with a combined 33.8% for petrol and diesel vehicles.

Key Highlights

- The largest number of EVs in 2025 was sold in Germany: 856,540 vehicles were purchased, up 49.61% from 2024.

- The Nordics continue to lead Europe in the transition to electric mobility, with 97.41% of newly registered cars in Norway now fully electric.

- EVs account for 71.08% of new cars sold in Denmark, 63.19% in Sweden, and 61.32% in Iceland.

- Europe’s electric vehicle market expanded in 2025, with total sales rising 30.91% from the previous year to 3.86 million units.

To outline which nations in Europe are leading or falling behind in the shift to electric mobility, our team at TradingPedia analysed EV sales using new car registration data from the European Automobile Manufacturers’ Association (ACEA) for January-December 2024 and 2025. We also examined the top-selling EV brands using CleanTechnica’s January-November sales reports. The full dataset is available on Google Drive via this link. The full dataset is available on Google Drive via this link.

Europe’s EV landscape in 2025 reveals a disconnect between total sales and per-capita adoption. Germany, the United Kingdom, and France led the market with 435,549 to 856,540 new EVs sold last year, yet their adoption relative to population tells a different story. Germany ranks 9th and the UK 8th per capita, while France falls to 16th with 653 EVs per 100,000 people. By contrast, smaller markets like Norway and Luxembourg register the highest per-capita adoption, with 3,096 and 2,383 EVs per 100,000 inhabitants, highlighting how population size and market scale can mask the pace of EV uptake.

Here are the European countries with the most EV sales per 100,000 people (2025 totals):

- Norway - 3,047 BEV + 49 PHEV = 3,096 EV sales per 100K

- Luxembourg - 1842 BEV + 541 PHEV = 2,383 EV sales per 100K

- Iceland - 1,488 BEV + 729 PHEV = 2,217 EV sales per 100K

- Denmark - 2,101 BEV + 78 PHEV = 2,179 EV sales per 100K

- Sweden - 932 BEV + 680 PHEV = 1,612 EV sales per 100K

- Belgium - 1,222 BEV + 336 PHEV = 1558 EV sales per 100K

- Netherlands - 846 BEV + 398 PHEV = 1,244 EV sales per 100K

- Germany - 652 BEV + 372 PHEV = 1024 EV sales per 100K

- UK - 677 BEV + 322 PHEV = 999 EV sales per 100K

- Austria - 666 BEV + 316 PHEV = 982 EV sales per 100K

Here are a few key takeaways from the report:

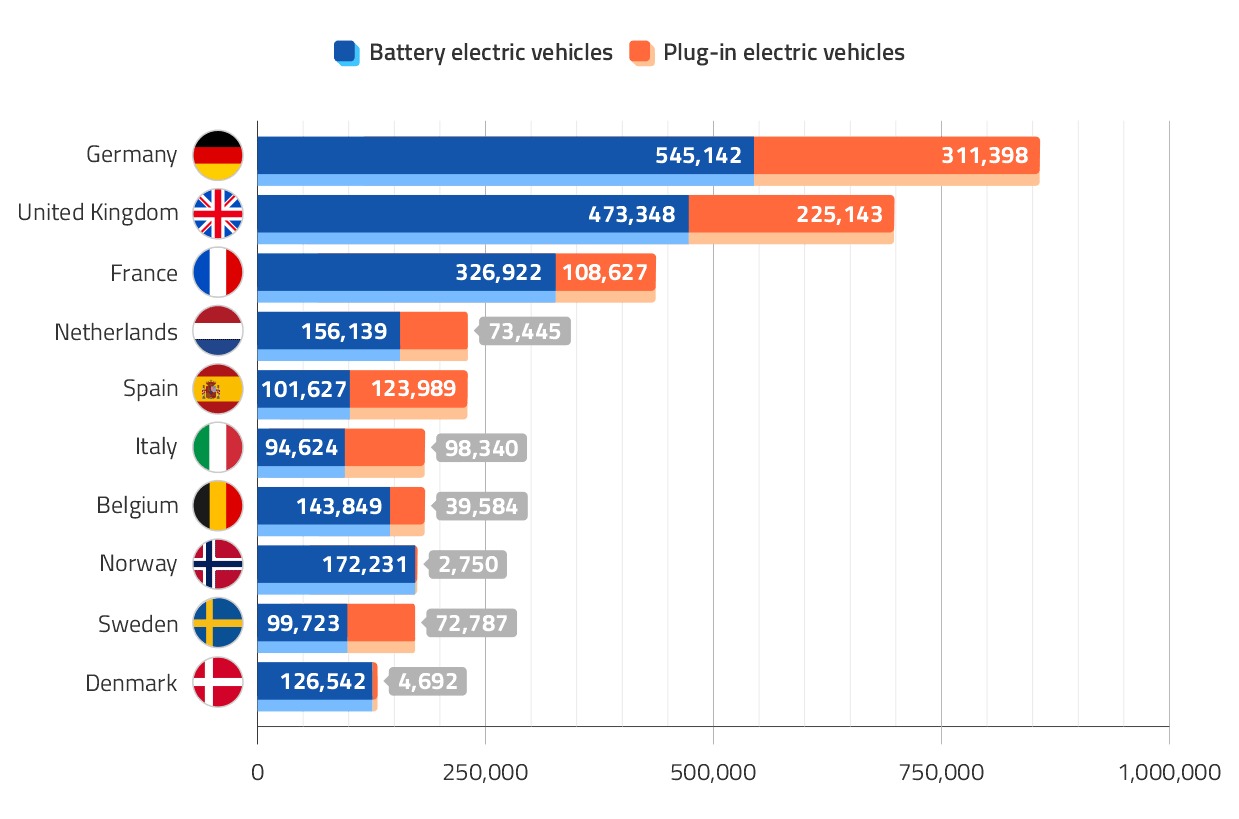

- In 2025, Germany led European EV sales with 856,540 new registrations, including 545,142 battery-electric vehicles (BEVs) and 311,398 plug-in hybrids (PHEVs). The United Kingdom followed with 698,491 units (473,348 BEVs and 225,143 PHEVs), while France registered 435,549 EVs (326,922 BEVs and 108,627 PHEVs), with the Netherlands rounding out the top four at 229,584 (156,139 BEVs and 73,445 PHEVs.) Germany’s EV sales surged over 49% year-on-year, the UK grew by 27%, and the Netherlands saw a 24.2% increase. France was the only major market to experience a slight decline, with overall EV registrations falling 0.3%, driven by a 25.8% drop in PHEV sales.

- On a per capita basis, the picture shifts markedly. Norway leads both in EVs per capita, with 3,096 per 100,000 citizens, and in the share of EVs among new registrations, exceeding 97%. Luxembourg follows with 2,383 EVs per 100,000 inhabitants, while Iceland and Denmark register 2,217 and 2,179 units per capita respectively. At the lower end of the spectrum, Bulgaria and Romania sold just 45 and 47 new EVs per 100,000 people, with both countries recording a very low share of EVs among new car registrations, under 7%.

- EV sales grew most sharply in Poland (+141%), Lithuania (+119%), and Latvia (+115%), though their share of total new car registrations in 2025 remained relatively modest, between 12% and 19%. By contrast, Malta (-16%), Estonia (-12%), and Romania (-10%) saw declines in EV registrations. Belgium also recorded a 5.6% drop, largely due to a more than 40% decrease in plug-in hybrid sales, even though the country ranks 8th in Europe for EV market share at 44.23% and 7th in total units sold, with 183,433 vehicles.

- In 2025, Europe’s new car market continued its shift toward electrification, with hybrid electric vehicles (HEVs) leading sales at 4,566,850 units, representing 34.4% of total registrations. Battery-electric and plug-in hybrid vehicles combined (EVs) accounted for 3,858,088 units, or 29.1% of the market, surpassing petrol cars, which totaled 3,467,041 units (26.1%). Diesel vehicles made up just 7.7% of new registrations, while cars powered by other fuels contributed 2.7%.

‘Europe’s EV transition is now about more than just sales volume; it is being shaped by strategic industrial policy and emerging regulatory norms. The push by major automakers for CO₂ bonuses and ‘Made in Europe’ incentives reflects industry concern about competitiveness and a desire to secure domestic manufacturing in the face of rising imports and global competition. At the same time, recent moves abroad - such as China’s decision to ban flush, electronically actuated EV door handles in favour of mandatory mechanical releases for safety reasons - signal that regulators are tightening scrutiny on EV design and safety standards, and could influence how vehicles are engineered for global markets.The combined effect of these trends suggests that Europe’s EV market will be driven as much by regulatory direction and industrial strategy as by consumer demand, and that harmonising policy on incentives, safety, and production localisation will be crucial if the region is to maintain momentum and avoid uneven adoption across member states.‘